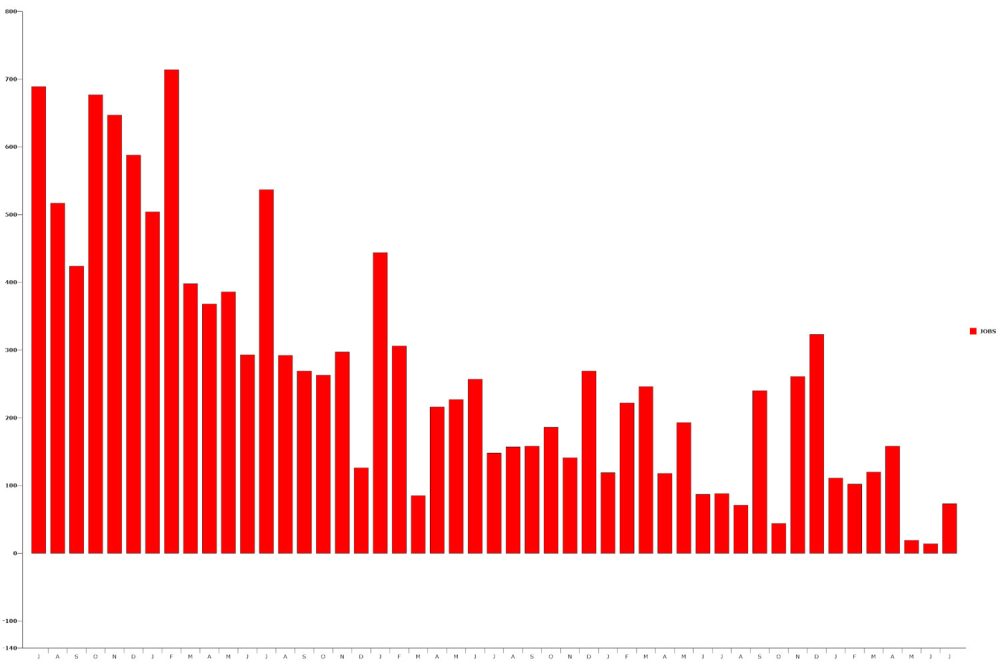

It was the worst quarter for job creation since the enormous employment losses in April 2020 when COVID shut down most of the economy. The national economy added 73,000 jobs in July and 106,000 jobs in the prior three months combined. The jobless rate increased marginally to 4.2. Over the last 14 months, it has remained in the range of 4 to 4.2 percent.

In May and June, the Bureau of Labor Statistics had first reported that 144,000 and 147,000 jobs, respectively, had been created. In an exceptionally drastic change, it reduced those numbers today to just 19,000 in May and 14,000 in June, resulting in the loss of 258,000 jobs. The average monthly job creation under the president’s watch so far this year has been 85,000, which is half of the 168,000 jobs created during the final year of the Biden administration. In addition to the ongoing, deliberate loss of employment in the federal workforce, other factors contributing to the slowdown include tariffs, increased interest rates, and employer uncertainty.

According to the federal court system, filings for personal and company bankruptcy increased nationwide by 11.5 percent in the 12 months ended June 30 compared to the prior year. Bankruptcies in Florida increased from 18,471 last year to 23,442 in the last 12 months, a 23 percent increase statewide and a 27 percent increase in the Middle District, which includes Flagler County.

According to Flagler Beach bankruptcy lawyer and city commissioner Scott Spradley, the trend for bankruptcies has been on the rise and will likely continue to rise over the next few years. There are several explanations for this. Covid is the cause of one of them. Many people were either unemployed or underemployed at that time. They depleted their funds and accrued debt from their credit cards. Many have just been unable to keep up, especially with credit card debt, which has significantly increased the number of bankruptcies.

According to the Federal Reserve, household debt reached a record $18.2 trillion in the first quarter of this year, of which $5 trillion was unrelated to mortgages. Credit cards accounted for $1.18 trillion of that total, representing a $67 billion rise from the previous year.

According to Spradley, the labor pool has shrunk and is continuing to shrink due to the expulsion of undocumented immigrants, and companies have had difficulty hiring qualified workers, which has led to a rise in corporate bankruptcies.He claimed that he is witnessing an increasing number of families as a last resort rather than as a result of lavish spending.

Families and businesses have experienced more challenges as a result of the substantial number of layoffs, whether they are from the government or companies connected to government agencies, according to Spradley. Unfortunately, it appears to be a pattern that will last for a while.

With the loss of 12,000 positions in July, federal government employment has now fallen by 84,000 since peaking in January. Workers are considered employed even if they are on paid leave or receive continuous severance pay. Social assistance (18,000), individual and family services (21,000), and health care (50,000 employment) saw the most job growth during the month, while other sectors saw no growth at all. Manufacturing, the very industry that the Trump administration said tariffs would help, lost 11,000 for the third consecutive month. Tariffs have instead raised the price of raw materials.

The average tariff, which is essentially a charge on all imports, is 15% now as opposed to 2% at the start of the year. In other words, a $100 item now costs $115 when import duty is added, compared to $102 in January.

At the end of next week, even higher tariffs are expected to take effect.

Due to economic factors, such as reduced full-time hours or inability to secure full-time employment, 7.2 million people were unemployed and an additional 4.7 million were working part-time. 6.2 million more people are not in the labor force but are looking for work; they are not included in the unemployment statistics. nearly the past year, that number has risen by nearly half a million. 7.9 percent is the alternative unemployment and underemployment rate, which takes into consideration individuals who are unemployed, discouraged workers who have left the workforce, and those who work part-time for financial reasons. A quarter of the unemployed had been unemployed for six months or longer.

Despite this, the Conference Board reports that consumer confidence increased slightly in July. According to Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board, consumer confidence has leveled down since May after plunging in April but is still below its peak from the previous year. In July, there was a minor uptick in overall confidence as future pessimism subsided. The recent data suggest that the recovery might not last long.